“The Misdiagnosis of Obamacare” was co-authored by Benjamin Duong and Chelsea Hazlett.

Healthcare insurance, like any insurance, is a gamble. But unlike other types of insurance, there is more on the line with this gamble.

Perhaps you decide to pay the often hefty premiums that eat up your income and never need healthcare insurance beyond routine checkups. Or perhaps you forgo insurance altogether, but find yourself hospitalized by an accident or cancer or some other disease and you’re steamrolled by catastrophe level hospital bills that leave you dead on the water with debt.

In America, you are guaranteed emergency-room treatment. But beyond that, there’s no guarantee to all-encompassing medical care because medical treatment is a private good, and private goods aren’t free.

Even with emergent care, hospitals have the right to try to saddle you with the full bill afterwards.

Via: Gstatic

And so we come to the issue at hand: Obamacare.

Officially known as the Affordable Care Act, Obamacare is the crowning policy push by President Barack Obama and his administration. It is an attempt to reform one side of healthcare: the issue of ensuring coverage, guaranteeing, in some manner, that every American will have a way to cover a majority or all of any healthcare bill.

For over half a decade now, we’ve been treated with national news about Obamacare and its rollout — some of it good, but most of it bad.

The condensed version of the bill was 1,000 pages. Its rollout was a near-disaster. And implementation has faced dozens of delays and repeal attempts and had to survive several court challenges.

The bill is complex, and by their own admission, even congressmen don’t entirely know what’s going on with Obamacare. Understanding Obamacare is a colossal task.

We’re here to change that.

Here, we will breakdown and simplify everything you need to know about Obamacare — how it came to be, why the bill and its rollout were flawed, what it means for you as a patient and what it means for the future of healthcare in America.

Healthcare Reform in America: An Abridged History

America has had a firm, derogatory view of socialism for almost a century, beginning with the First World War and its accompanying “anti-German fever.”

This disdain carried over to healthcare methodology, and so the legislation of required health insurance was shot down even in 1917 to adhere to the American fear of Communism.

Aside from considering it a socialist piece of legislation, one common misconception associated with Obamacare is the belief that the functionality of U.S. healthcare is a new problem.

After 1917, the question of healthcare and health insurance was left to individuals. But during the Truman era, which spanned the latter half of the 1940s up to 1953, a decision set America on a path in a distinct direction away from universal healthcare, while other countries turned towards it.

During WWII, the IRS decided that health-insurance benefits could not be taxed as wages.

Therefore, a massive tax loophole was born for unions, who could now incentivize membership. With healthcare now in the hands of employers and unions, the idea for universal healthcare was killed off once again. A combination of unions, companies, hospitals, and a vehement American Medical Association lobbied hard against healthcare reform, and this effort after WWII established a long tradition of business opposition to universal healthcare.

Fast-forward to when Bill Clinton was in office in the 1990’s. The lady of the house, Hillary Rodham Clinton, was appointed with the task of augmenting healthcare reform.

The resulting “Hillarycare plan” was incredibly complex.

Its general idea was that the government would regulate insurance-buying cooperatives and likely force people to give up the healthcare insurance they had at the time. Small businesses, which are a significant portion of employment, have little resources and expertise to properly purchase insurance for themselves, and when they do, their insurance premiums are often higher than those of large corporations. Insurance-buying cooperatives allow several small businesses to pool together and buy insurance at favorable rates.

It didn’t go over too well.

Republicans and the healthcare insurance lobbyists decried the attempt to intrude in the affairs of small businesses, and Congress killed Hillarycare. The initiative was faulted for losing the House of Representatives to the G.O.P. after decades of Democratic majority.

Another common misbelief about Obamacare is that it’s a Democratic or liberal idea.

In reality, the bill was based off of Romneycare, Massachusetts Governor Mitt Romney’s healthcare reform plan. (And yes, this is the same Mitt Romney who ran for president in 2012.)

Via: Ebony

Romneycare established a “three-legged stool” foundation. The three legs were: reform of the individual insurance market; forbidding insurance providers from screening individuals for pre-existing conditions (therefore, eliminating any reason for Massachusetts residents to not have health insurance, and penalizing those who did not buy in); and address those who cannot afford insurance.

All of this became the primary basis of Obamacare. [America’s Bitter Pill – Steven Brill]

So in terms of policy, we know the history. But what are the intentions of Obamacare?

Intentions and reality seem to differ.

Affordable Care Act Says What

The 2008 presidential election was dominated by two major issues: the financial crisis, which later led to the Great Recession, and healthcare reform.

The financial crisis would inevitably be dealt with through several massive government bailouts, but healthcare remained the chief mandate of the Obama administration.

Government spending on healthcare was growing out of control, and medical costs were hitting all-time highs. Coupled with the fact that it became impossible to ignore the millions of uninsured Americans, President Obama pushed forward with his mandate to pass healthcare reform.

Deciding to base his bill off of Romneycare, which ostensibly should’ve made Obamacare more palatable for Republicans, President Obama built upon Romney’s three-legged stool to construct the Affordable Care Act.

After several years of policy writing, political negotiations, backroom deals with the insurance and healthcare industries, and congressional machinations, the Affordable Care Act was passed on March 23, 2010.

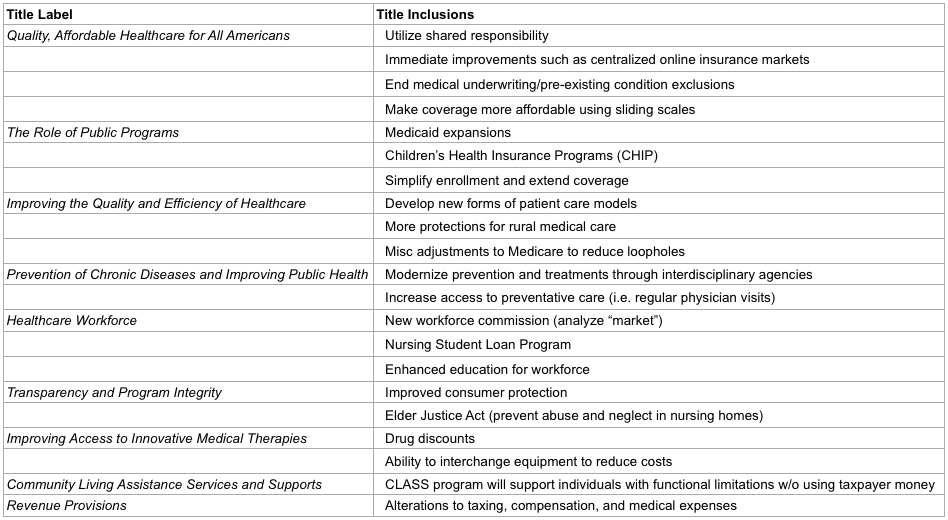

In the following table, we breakdown the essential elements of Obamacare — all several thousand pages of the bloated bill, condensed into an easy read and broken up into the nine main sections of the bill itself.

Chelsea Hazlett

The overall bill mainly seeks to ensure expanded coverage access for Americans.

Along with the ‘“three-legged stool,” the bill places some mandates and incentives to modernize healthcare and to protect consumers. Beyond that, there are a few sections that attempt to reduce some costs, for both patients and the government, but the cost-side of healthcare remains largely untouched.

Needless to say, any time politics are involved, you end up with so many figures stirring the pot in an attempt to be re-elected that any good act or bill risks souring. The intentions of Obamacare are positive but in the world of Washington, these intentions have been diluted and implementation has been messy and slow.

The Rolling Stumble

Unanticipated roadblocks are a typical occurrence when implementing an act.

The rollout of Obamacare was no exception. It can be viewed as a failure partly because of a lack of foresight. However, most of the blame falls on poor planning.

The legislative process partially hindered the enactment of Obamacare. Though signed into law in 2010 after an already lengthy battle, the law continued to be written and rewritten by the executive and legislative branches for three and a half years, with 51 significant changes thus far.

Most of the discord comes from ideological differences between political parties, but by 2013, everyone was up in arms, believing that President Obama was overstepping his executive-power boundaries.

Meanwhile, outside of Capitol Hill, the rollout of Obamacare was largely unsuccessful as the infrastructure of Healthcare.gov was lacking.

The company that was contracted to establish HealthCare.gov failed miserably to deliver. The online federal health insurance marketplace was supposed to handle up to 250,000 visitors a day but crashed after 10,000.

Kathleen Sebelius, former Secretary of Health and Human Services, suggested that the “technical failures [were due] to the fact that the administration didn’t know until 6 months before enrollment which states would be building their own sites and which would be using the federal site.”

Via: Washington Post

Kentucky was one of the states who chose to build their own version of Healthcare.gov.

It functioned seamlessly, thanks to rigorous beta testing and contingency plans. Several glitches during rollout were easily isolated and fixed. Its implementation team worked in sync, and communications and task delegations were clear ["America’s Bitter Pill" - Steven Brill].

Healthcare.gov, on the other hand, underwent minimal testing and lacked a backup strategy of any kind.

Moving past these primary malfunctions, the new question was how to get Obamacare to function within (and above) the realm of Medicare and Medicaid.

Crying Medicare Foul

Medicare and Medicaid work by reimbursing or subsidizing the cost of medical treatment by paying after the fact.

Patients get the care they need, and the government cuts down the bill from the hospital.

Through Obamacare, a backroom deal negotiated by hospital lobbyists would allow Obamacare to reduce increases to Medicare payments (without a fight) in return for the millions of newly insured patients.

However, due to the nature of Obamacare, the bill quickly became a scapegoat for everything wrong with healthcare, regardless of whether Obamacare was actually at fault.

News headlines showed hospitals in a “panic” over the future reductions to Medicare payments that would increase over time. They blamed the Medicare reductions for their need to cut staff and treatments. Besides the fact that they would be losing Medicare payments in return for a massive new revenue source in the form of millions of new patients (a deal they specifically made themselves), the hospitals crying foul play about these reductions neglected to mention that hospital executives and administration saw little to no cuts to their own pay.

With most of these execs making well into the millions, many even saw their personal profits rise.

Obamacare’s cuts to Medicare payments to hospitals will not harm patient care.

In fact, new studies have shown that hospital productivity could grow more quickly than the schedule of Medicare payment reductions. Patients will get better care, the government will have to pay less to hospitals, and combined with more people being covered with healthcare insurance, everyone technically wins.

Complaints by congressmen and hospital groups about Obamacare, on Medicare payment reductions, are little more than political scapegoating.

Furthermore, new programs under Obamacare, including the Accountable Care Organization (ACO) and expansion of use of electronic medical records, should help hospitals improve quality of care while spending less. The ACO specifically will set optimal quality and cost levels for hospitals and providers, and will set out to offer bonuses for successes and penalties for failures. As least in this aspect, Obamacare should be a boon to the healthcare industry and patient care, not the reverse, as claimed by critics of the healthcare bill.

This does not excuse the reality that Obamacare was constructed through backroom deals with the healthcare and insurance industries.

The hundreds of lobbyist groups that swarmed the bill all worked to insure that the proposed reforms would not severely hurt their profits.

The result was a bill that got its job done but could’ve been much better. Furthermore, the bill highlights the extreme power of lobbyists and moneyed interests in Washington, and this power is why the bill only addresses coverage of healthcare, not the costs, which we will later address.

Lie of the Year

Headlines blazed with the broken promise of President Obama.

His promise to the American people, “If you like your healthcare plan, you can keep your healthcare plan,” turned out to be hollow.

About 2 percent of insurance plans were canceled because they failed to meet the standards of Obamacare, and there were dozens of stories in the news of people losing their favored plans.

President Obama misled the public.

But here’s the thing, those insurance plans that were cancelled, were cancelled for a very specific reason. They were effectively junk plans. The reason those people liked those plans was because they had very low premiums. But when it came down to it, this paltry breed of insurance covered little more than routine check-ups and were useless in dire straits.

So, technically speaking, President Obama lied. But Obamacare’s insurance standards are necessary to enforce real, useful insurance.

Although the implementation of the Affordable Care Act was almost a miserable crash and burn, it isn’t a failure altogether. There are clear, tangible results.

Nearly 30 million Americans have gotten health insurance under Obamacare and the number of uninsured adults has dropped from 18 percent to 12.3 percent between 2013 and 2015.

Yet 43 percent of American’s have an unfavorable view of Obamacare — though an overwhelmingly large percent favors its major components. There is an obvious political toxification of the term “Obamacare” that is hindering understanding of the bill.

A collective effort to bridge the gap between suggestions and reality is necessary if healthcare reform is going to work in the United States.

The Infamous King v. Burwell

Having already successfully dealt with the Supreme Court challenge to the individual mandate policy, Obamacare faced another challenge in the Supreme Court in 2015.

This time, the challenge revolved around a mistake in wording in the bill, one that would potentially limit government subsidies for healthcare to only those states that established their own state-run healthcare exchanges.

With few states having successfully done that, the ruling had the potential to leave millions without needed subsidies for healthcare insurance, which would lead to a collapse in the insurance markets and a dramatic increase in premiums as a result.

Via: Ncadp

On June 25, the Supreme Court ruled in favor of Obamacare, with the 6-3 majority ruling noting that the intention of the bill was never to cripple itself, thus allowing the bill to take a change of interpretation to reflect that intention.

With this ruling, Obamacare moved past its last major legal hurdle and is now a solid fixture in healthcare law.

Though the healthcare law will move on as planned, there appears to be one possible change to the nature of the law due to the SCOTUS ruling.

Now it appears that healthcare insurance consumers can expect to receive the same subsidies from the government, regardless of whether they get their insurance through a state-run exchange or the federal exchange.

States, many of which have had spectacular failures in setting up their own exchange from scratch, might use this ruling to simply forgo their own exchange.

This will have no negative bearing as HealthCare.gov is now finally running smoothly, but states opting out of their own exchanges does take away from the customizability of state exchanges that Obamacare had hoped states would utilize.

College and Health Insurance

In accordance with the Affordable Care Act, the University of Florida made it mandatory for students to have health insurance in 2014 to reduce the number of college students who are uninsured (the largest proportion of uninsured people overall).

For undergrads, a provision within Obamacare allows individuals under the age of 26 to remain on their parents’ health insurance policies.

But for those of us whose parents do not have health insurance, UF began referring students to a United Healthcare Student Resources program, which was pretty “eh,” speaking from experience.

Graduate students have their own GatorGradCare, which is through Florida Blue (although they do have to enroll).

Overall, the impact of Obamacare on college students seems to be minimal as financial aid can even be used to cover health insurance costs. So acting proactively (even if you were forced to) is probably in your best interest here.

Broken Bones: The Cost Side of Healthcare

Americans demonize socialism, as mentioned earlier, and there are some relatively socialist aspects of Obamacare. But if put on a political ideology spectrum, with capitalism on one end and socialism at the other, it would fall square in the middle.

It is indeed a regulated free market, but it does take care of the free-rider problem, meaning that people who do have health insurance won’t have to pay more for those who don’t and will therefore lower the cost of healthcare for everyone.

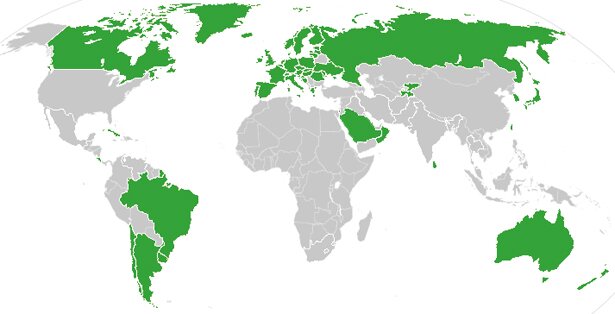

Truly socialist healthcare systems do exist in places like France, Canada, Russia and Australia. Though tax rates are high to pay for the free healthcare, these systems (combined with cost controls) have established healthcare as a complete basic right

The U.S. is one of the few developed nations that lacks universal healthcare, and it seems to be working out pretty well for everyone else but us.

America spends more per capita than all other economically developed countries besides Norway and the Netherlands on healthcare but seem to be relatively less successful in its spending.

Sweden’s healthcare is considered the best in the world and it is completely socialist. All Swedes have equal access to healthcare under a decentralized, tax-payer funded system.

Via: The Atlantic

Universal healthcare is unlikely to come to America anytime soon.

But while Obamacare managed to address the coverage side of healthcare, the cost side was left almost entirely unaddressed. Medical industries are largely unfettered by regulations that control how much consumers can be charged.

And these costs continue to have an upward trend.

Without placing limits on the cost curve we can expect that within a few decades we will be dealing with another healthcare crisis that will very likely throw us into fiscal doomsday. With this understanding, we decided to make our policy suggestions along the lines of the capitalistic practices that Americans love so dearly.

These policy suggestions are precisely what was recently suggested by journalist and writer Steven Brill in his book, “America’s Bitter Pill.”

Super Hospitals

Brill suggests a complete takeover by oligopolies. Let hospitals absorb all aspects of healthcare — labs, clinics, doctors, insurance and other hospitals themselves — he says.

To the average American, this sounds like a nightmare. But as Brill explains, this is an effective method for optimizing healthcare.

Allowing hospitals to absorb every functional part of healthcare eliminates middlemen, thus cutting out huge swathes of unnecessary costs — everything, including the abysmal industry of insurance, will fall under hospital control.

Having hospitals take over insurance practices in particular will go a long way toward cost control. The extra costs of unnecessary practices would fall on hospitals themselves, rather than third-party middlemen, therefore disincentivizing inflating treatment costs and over-treating or over-testing patients.

Brill further advocates for establishing competition for full treatment of patients rather than piecemeal treatment.

Under the current system, most hospitals use a chargemaster to tally up charges for patients for each element of their treatment. A charge for one test, a charge for a pillow, a charge for another test, a charge for an IV, etc. Instead, Brill wants to establish transparent, whole treatments at a flat-rate with no bill padding.

This would force health systems to compete for better whole care, which would be infinitely better for patients.

After all, we are whole human systems, not individual little problems that merit separate charges.

Via: Snoopwall

But what would prevent hospitals from abusing all this newfound power? Brill addresses this with a set of nonnegotiable regulations for these super-hospitals:

Oligopolies

- Allow hospital brands to establish oligopolies, but maintain clear anti-trust laws to prevent monopolies

Profit Caps

- Cap operating profits at around 8% (we let oligopolies exist in return for cutting down profits) – possibly establish an excess profits pool to be used to back struggling hospitals in small markets, such as rural areas

Salary Caps

- Cap total salaries and bonuses paid to any hospital employee who does not practice full-time medicine at 60 times the amount paid to the lowest salaried full-time doctor (i.e. a first year resident being paid $50k would limit an exec to $3 million, which is still a lot, but for many execs this would amount to a large pay cut)

Embedded Advocacy

- Streamline the appeals process with an embedded staff of advocates and ombudsmen in each oligopoly company (allowing patients to appeal if they didn’t receive proper care, and allowing doctors to claim if they are being forced to skimp on care to cut costs)

Doctor-Leaders

- Mandate all oligopolies to have its actual CEO a licensed physician who has practiced medicine for a set minimum amount of years (this would bind hospitals to patient care, and not to pure profit making, establishing patient-centered work culture)

Medicaid Discounts

- Require any sanctioned oligopoly integrated providers to insure a percentage of Medicaid patients at a stipulated discount

Death to the Chargemaster

- Require any sanctioned oligopolies to charge any uninsured patient no more than they would charge any competing insurance companies they accept, or if they only accept their own insurance, at a price based on their regulated profit margin – i.e. completely eliminate the chargemaster

Already several hospital systems have made strides toward making these changes themselves. But it is not enough, and it is not fast enough.

Let us empower more doctor-leaders to take the reins from profit executives and establish patient-centered hospital cultures.

Let us allow hospitals to engage in industry takeover in order to eliminate all middlemen and bring about the end of the insurance companies that hold patients and the government hostage.

Let us eliminate incentives for the healthcare industry to inflate costs.

And finally, let us finally establish profit limits on the industries that provide us with medications and medical tech.

The healthcare industry will still make all the profit in the world, but it is time to end their robber baron practices.

Although we have made a massive stride toward complete coverage through Obamacare, if we don’t establish measures like those suggested by Brill, Americans will face a massive fiscal crisis.

Obamacare is Here to Stay

Three elements of Obamacare will go into effect over the next five years.

By 2018, a 40 percent tax rate will kick in for insurance companies who continue to provide “Cadillac” health plans ($10,200+ for individuals, $27,500+ for families).

The current law has a gap between $2830 and $4550 where Medicare doesn’t cover the out-of-pocket costs of drugs for seniors. By 2020, this so called “doughnut hole” will be eliminated, and seniors will continue to pay the normal 25 percent of drug costs until they reach a catastrophic Medicare level where their co-payments will drop to just 5 percent.

With those last three policies, Obamacare will be in full effect.

Everyone can potentially benefit from the practices set forth by President Obama’s Affordable Care Act. But before we can get there, the cost side of things must be addressed.

We believe that our policy suggestions actually fit into what Obamacare stands for and would address the side of healthcare that Obamacare did not: the rampant and growing cost side of healthcare. But in terms of what is tangible, we hope this piece stands as a satisfactory analysis of what has been and what should be.

Americans will see continued improvements across the board because it isn’t simply a push toward universal healthcare — it is a panacea to our medical-industry maladies.

Featured photo courtesy of: Wikimedia

Pingback: On The Issues: Marco Rubio - Tampa Bay SceneTampa Bay Scene()